vs Traditional Credit Repair

vs Traditional Credit Repair

| FEES | Traditional Credit Repair | |

|---|---|---|

| Setup FEE | $0 FOREVER | Up to $399 (One Time Fee) |

| Monthly FEE | $0 FOREVER | Up to $199 (Monthly) |

| Credit Monitoring | $29.95 MONTHLY | $25-$40 (Monthly) |

| Average Monthly Cost | $29.95 | $250+ |

Easy to Get Started

Start Rebuilding Your Credit Today

Let’s be honest, you can do it yourself, well, if you absolutely love tedious, brain-boggling work. Said no one ever. We know you have better things to do, so that is why we created the Repair for Free credit automation. Our easy to use, simple to understand, technology is FREE. You only have to cover the cost for your credit reports.

Start Your Repair for Free Journey

Your enrollment is quick and easy! WIth a few clicks you will be enrolled and have your credit reports imported into the system.

Unique Dispute Letters

The system will analyze your credit reports, create custom dispute letters and even mail them for you within minutes.

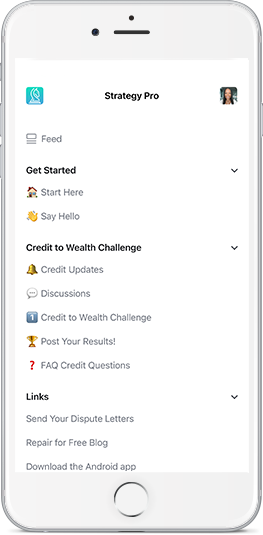

You are Invited!

Once you accept your invite, you will have access to the credit building community where professional coaches will share with you tips, tricks and hacks to improve your credit quickly

Access Private Community & Coaching App

You will not have to do your credit repair journey alone! Once you sign up and import your credit reports, you will be invited to join our FREE inner circle to access credit building courses and have access to our coaches.

Access to Coaches

Get access to coaches who have literally used their credit to build real estate and business empires

Credit & Financial Courses

Finally understand how to optimize and leverage your credit with easy to follow credit & financial courses

Discussions

Interact with the community and coaches in our community rooms

Credit Building Tools

Vetted list of positive accounts that will help you build a strong credit profile

Live Trainings

Live trainings & Q&As to get your burning credit questions answered

Share Your Success

Celebrate any deletions or credit score increases with your tribe

Why is it Free

We believe that better credit can solve bigger problems. We walk you through the process and help as long as you need us. The only thing we require you to pay for is a credit monitoring subscription. As we work towards your financial goals, we also recommend credit-building offers like credit cards and loans. If you choose any of these tailored offers, the providers compensate us.

How it Works?

Process to Getting Started

Yes, you got this! No more wasting your valuable time trying to decipher your credit reports or keep track of your reports and letters. We can manage it all for you and it’s free! Just purchase your credit reports through our partner credit monitoring provider!

Step 1. Get Started

It’s easy and only takes a few minutes. First, click the get started button, register, and authorize the technology to show you all your info. With our fully online enrollment process, there are no pesky sales calls!

Step 2. Credit Report

Next, continue to follow the steps to order a copy of your credit report. Once your report is ordered the Repair for Free system will analyze and identify your negatives.

Step 3. Select Items & Send Letters

Choose the items you want to dispute. The system will create your custom dispute letters and it will mail them for you!

Step 4. Build & Optimize Credit

Join the free coaching app to access credit building products (loans, credit cards, etc) that may meet your financial goals and expand your credit profile.

Step 5. Sit Back & Relax

When the credit bureaus receive your sent letters, they will conduct an investigation of the items you challenged.

Step 6. Results

Your results should arrive within 30 days or so. If your credit report still has errors, log back in and review your reports to see the next steps to getting the inaccuracies corrected.

Step 7. Repeat

If the errors are still on your credit report, you can apply more pressure with advanced disputing methods and utilize the systems follow up letters.